Facebook famously dropped its “move fast and break things” mantra in 2014, after which people realised it might have already cracked a number of things, Australian journalism included.

Yet, its latest foray into digital currency feels like a hark back to this mantra because it could do just that; disrupt the finance sector and in doing so turn Facebook from a platform reliant on advertising revenue, to a financial institution.

Last week Facebook revealed its plans to launch Libra next year alongside 27 other brands including Mastercard, Spotify and Uber which make up The Libra Association. Its vision for Libra is to create a truly global currency with the altruistic vision of bringing low-cost banking to billions across the globe.

But the real interest in the scheme for the social media giant is in the digital wallet, Calibra.

Calibra will exist as a standalone app and be built into Whatsapp and Messenger, making the process between seeing an ad and transacting a purchase, from anywhere around the world, seamless.

“If more commerce happens, then more small businesses will sell more on and off platform, and they’ll want to buy more ads on the platform so it will be good for our ads business,” Facebook’s head of Calibra, David Marcus, told CNBC.

But if Facebook can take a cut from all of these transactions that’s where the real value could be. While Marcus said the initial stage of Calibra will be to get people to actually use it, he flagged other services, such as loans, could be rolled out.

This could be a massive opportunity for the tech giant, which has already flagged developing countries, where traditional banks find it hard to reach people, as a key opportunity.

Will it be trusted?

Facebook knows its biggest obstacle isn’t the technology behind Calibra but trust.

Having The Libra Association, which aims to reach 100 members by launch date, govern Libra helps it assuage the public’s concerns about Facebook developing a currency.

It’s also created Calibra as a subsidiary of Facebook, also hoping to ease people’s concerns about handing their money to Facebook. Calibra has promised its users' data won’t ever be handed to the mothership, unless users decide otherwise:

“Aside from limited cases, Calibra will not share account information or financial data with Facebook, Inc. or any third party without customer consent. For example, Calibra customers’ account information and financial data will not be used to improve ad targeting on the Facebook, Inc. family of products.”

Marcus addressed the issue of trust, saying: “If people don’t want to trust us, they can use any of the other wallets that will be available. There will be plenty of competition.”

But when companies encourage competition, it’s usually because they don’t think there really is any. Although, like former shadow treasurer Chris Bowen telling people to vote against Labor if they don’t like the party's franking credit policy, they could be very wrong.

This hold on users is one of two advantages Calibra has in overcoming the trust issue and becoming mainstream. The other is slow regulators.

Facebook has 2.4 billion people in its ecosystem and despite on-going concerns around privacy these people aren’t going anywhere anytime soon.

Additionally, Facebook says it has no plans to plug in other digital wallets from competitors into its apps. This could give Calibra a head start. The more than two billion people across its platforms share messages and images, organise events and even shop. Adding payments and other financial services would be an easy extension too convenient for most users to pass up.

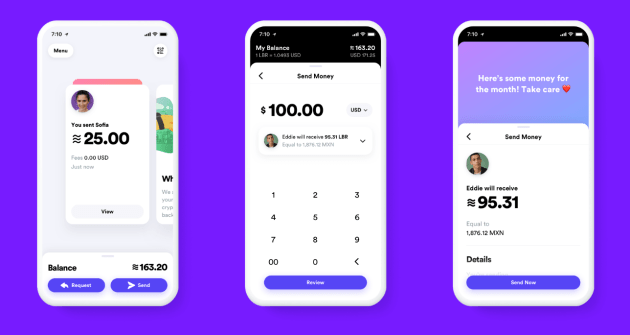

An early look at the Calibra App

China’s WeChat shows Facebook’s Whatsapp is ripe for internal payments, which Mark Zuckerberg is likely looking to replicate. And while Calibra won’t launch on Instagram, it’s easy to see it taking off on a platform which already has shoppable posts.

The second reason Calibra could be a success is that it may simply outpace regulators, hence why “moving fast” is in Facebook’s interest.

The Libra Association is essentially trying to build a global bank, but because it’s built on new technology, there aren’t any regulations in place to stop it, much like how Facebook and Google originally took off.

US Representative Maxine Waters asked Facebook to place a moratorium on Libra, and at the moment that’s all politicians can do. “We don’t have a regulatory agency to oversee who they are and what they’re doing,” Waters told CNBC. “This is like starting a bank without having to go through any steps to do it.”

Given how flummoxed regulators around the globe have been in dealing with big tech, Calibra will probably meet its launch date for 2020, and the other 100 members free to launch their own digital wallet may act as a defence in antitrust concerns.

Almost every sector has been “broken”, or at least shaken, by technology. Traditional media by social media, brick-and-mortar by e-commerce giants and transport by ride-sharing apps - finance could be next in line.

Regulation will start to roll in that impacts Facebook’s advertising business, although it’s unclear how significant this will be. The scrutiny Facebook is facing includes an investigation from the US Federal Trade Commission and the Australian Consumer and Competition Commission.

These regulations on the horizon are behind Zuckerberg’s push for a “privacy” focused app, one that acts as the world’s “digital living rooms”, not just its “digital town square”. Turning the app inwards, and turning itself into a secure, convenient financial service could work well for the company.

Have something to say on this? Share your views in the comments section below. Or if you have a news story or tip-off, drop us a line at adnews@yaffa.com.au

Sign up to the AdNews newsletter, like us on Facebook or follow us on Twitter for breaking stories and campaigns throughout the day.